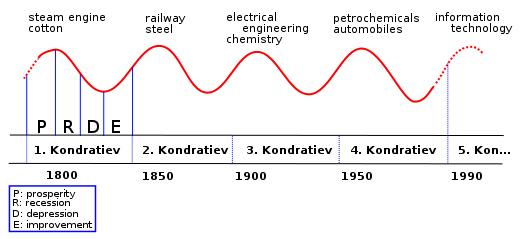

The monetary system is immensely complex these days, so as a thought experiment I like to imagine money away: ignore it altogether as it has no intrinsic utility itself. It merely directs the allocation of man power and resources, as a dictator might. But hopefully our system has more effective priorities: promoting the spread of useful innovations and keeping society healthy.

|

| Moai - 'Easter Island Heads' are misnamed, they've been buried to their shoulders by time. |

A conservative/neo-liberal might argue that rich people are no problem because they spend more, putting money back into the economy via the people they pay for products and services. However, I think the real problem is with the specific things they spend their enhanced incomes on.

Someone with 100 times more money than the average Joe doesn't buy 100 reasonably priced cars. Maybe they buy twice as many cars, but each one costs 50 times as much. It's actually quite difficult to spend that much money, so they will tend to purchase luxury items across the board, either impractically expensive versions of everyday goods or totally exclusive items like super-yachts.

Gucci handbags, jewel encrusted gold watches, $200M private yachts, giant mansions, hand made super-cars and fancy soirées are all about as useful at stimulating an increase in societal productivity as were the standing stones of Easter Island. For those unfamiliar: Moai (right) were erected all over the small Island as an expression of ancestor worship by clans. Making the statues took a heavy toll; there was total deforestation and ecosystem collapse. The isolated population of islanders had plunged from 15000 to 3000 by the time Europeans arrived in 1722. A 500% decrease, in under a century, with cannibalism. Shortly thereafter the 900 statues were toppled.

|

| The monolith erecting game is taxing indeed for the people of Nias Island, Indonesia, 1915. |